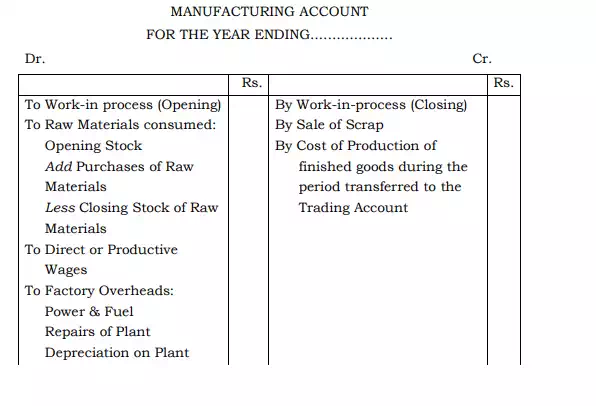

The concern which are engaged in the conversion of raw materials into finished goods, are interested to knowing the cost of production of the goods produced. The cost of the goods produced cannot be obtained from the Trading Account. So, it is desirable to prepare a Manufacturing Account prior to be preparation of the Trading account with the object of ascertaining the cost of goods produced during the accounting period.

The proforma of Manufacturing Account is given as under:

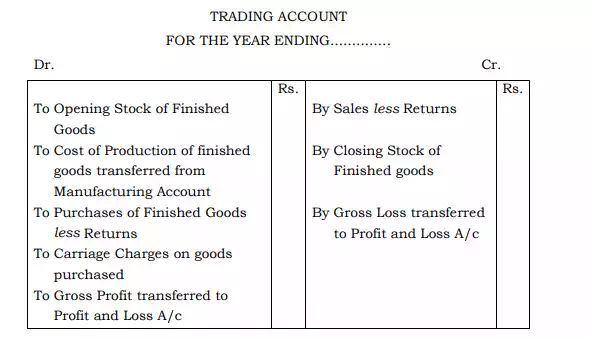

The Trading Account in case of manufacturers will appear as follows:

The gross profit or loss shown by the Trading Account will be taken to the Profit and Loss Account which will be prepared in the usual way as explained in the following pages.

Important Points Regarding Manufacturing Account

1. Raw Materials Consumed

The cost of raw materials consumed to be included in the debit side of the Manufacturing Account shall be calculated as follows:

Rs.

Opening Stock of raw materials ……….

Add Purchases of raw materials ……….. ………..

Less Purchase return of raw materials ………..

Less Closing stock of raw materials ………..

Cost of raw material consumed

2. Direct Expenses

The expenses and wages that are directly incurred in the process of manufacturing of goods are included under this head..

3. Factory Overheads

The term “overheads” includes indirect material, indirect labour and indirect expenses. Therefore, the term “factory overheads” stands for all factory indirect material, indirect labour and indirect expenses. Examples of factory overheads are: rent for the factory, depreciation of the factory machines and insurance of the factory, etc.

4. Cost of Production

Cost of production is computed by deducting from the total of the debit side of the Manufacturing Account, the total of the various items appearing on the credit side of the Manufacturing Account.

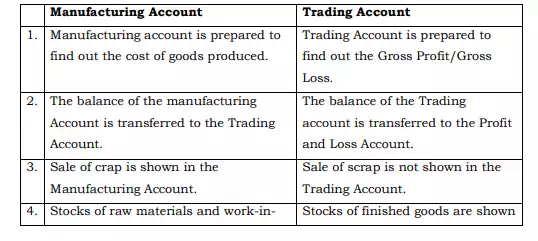

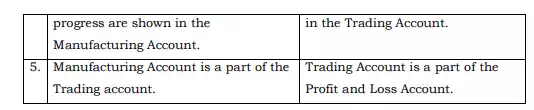

Difference between trading account and manufacturing account

{kind=link}